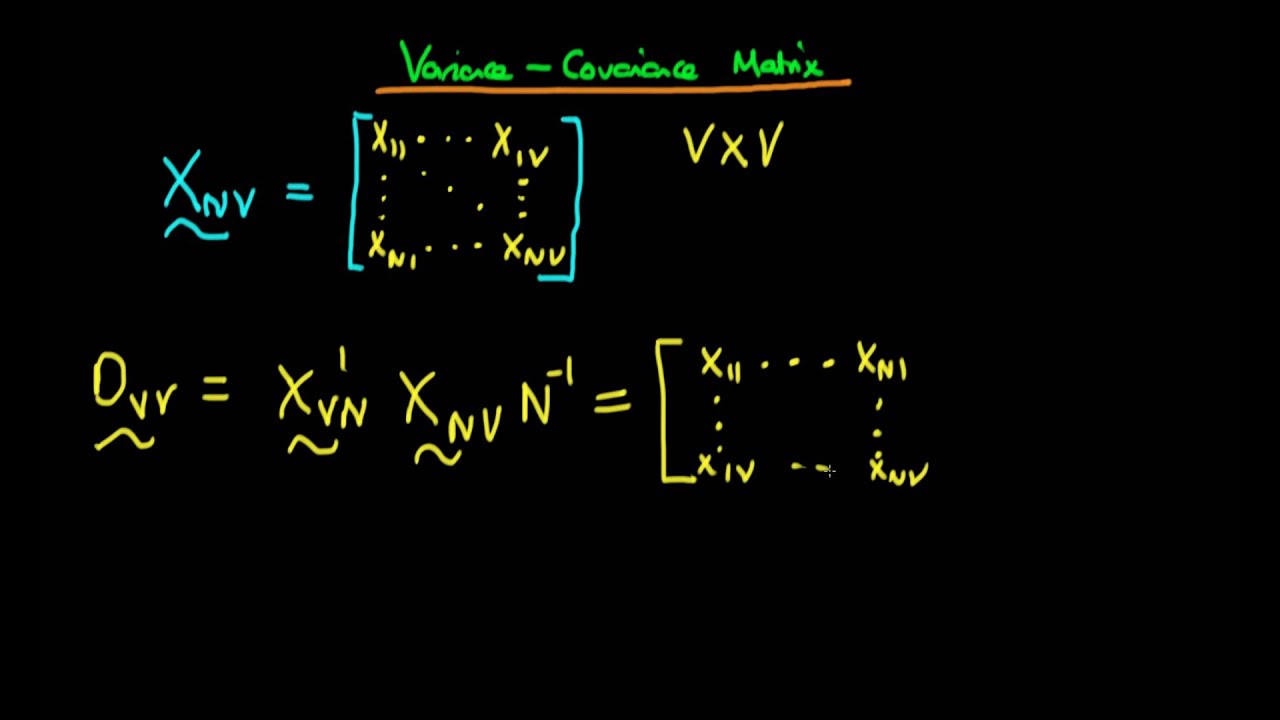

Cov Mat R Finance

Variance Covariance Matrix Stock Price Analysis In R Corpcor Covmat In 2020 Stock Market Crash Stock Research Stock Market

Rip Robin Williams Genie We Re Gonna Miss You T Shirt By Suzeejobs R Aff Ad Williams Robin Rip Genie In 2020 Geek Quotes Classic T Shirts Geek Humor

Album Cover Artist Book Project Launches On Kickstarter Album Covers Book Projects Album

Variance Covariance Matrix Using Matrix Notation Of Factor Analysis Youtube

Toyota Yaris Hybrid R Concept Mikeshouts Yaris Toyota Toyota Hybrid

Maxpider 3d Rubber Molded Floor Mat For Volkswagen Jetta 05 10 Kagu Gray Row 1 2 Jetta Gli Volkswagen Jetta Volkswagen

Smart beta is what people call algorithms that construct portfolios that are intended to beat market cap weighted benchmarks without a human.

Cov mat r finance.

Vtec Mini Vtec Mini Mini Cooper

Invitations De Mariage Fete Rock N Roll Design Disque Wedding Party Invites Affordable Wedding Invitations Rock N Roll Wedding

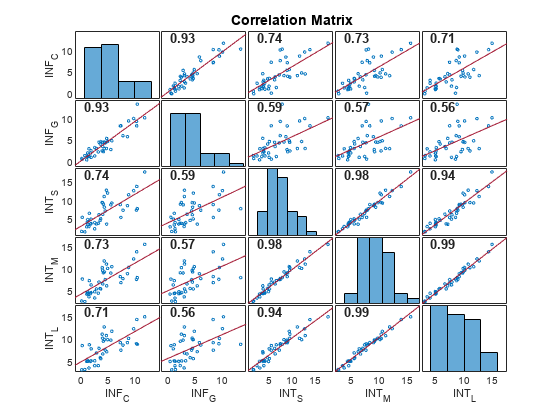

Plot Variable Correlations Matlab Corrplot

Fondos De Pantalla Simple Acrylic Paintings Aesthetic Pastel Wallpaper Aesthetic Art

Source : pinterest.com